When money is forced to “grow” on its own, it turns humanity into a perpetual borrower.

The Moral Foundations of Usury

The condemnation of charging interest on loans is not a modern invention; it is rooted in centuries‑old theological teaching. The Catholic tradition, for instance, labels usury a grave sin that corrupts the heart of exploiters. Pope Leo XIV explicitly warned that the practice reduces people to “objects of exploitation,” stripping them of dignity.

Even secular scholarship echoes this moral alarm. Kevin Considine, a theology professor, argues that usury “takes advantage of the needy” and therefore violates human dignity. The core objection is not the profit itself but the creation of wealth from nothing—a claim that the borrower never possessed. When a lender extracts value from a debtor’s future labor, the transaction becomes a form of exploitation rather than a fair exchange.

The Gospel Coalition notes that while the early church opposed all interest, later theologians distinguished between reasonable compensation for risk and predatory usury. Nevertheless, the line remains clear: charging excessive interest crosses the moral threshold. This ancient moral framework provides a lens through which we can evaluate today’s financial system.

How Modern Finance Turns Theory into a Daily Crisis

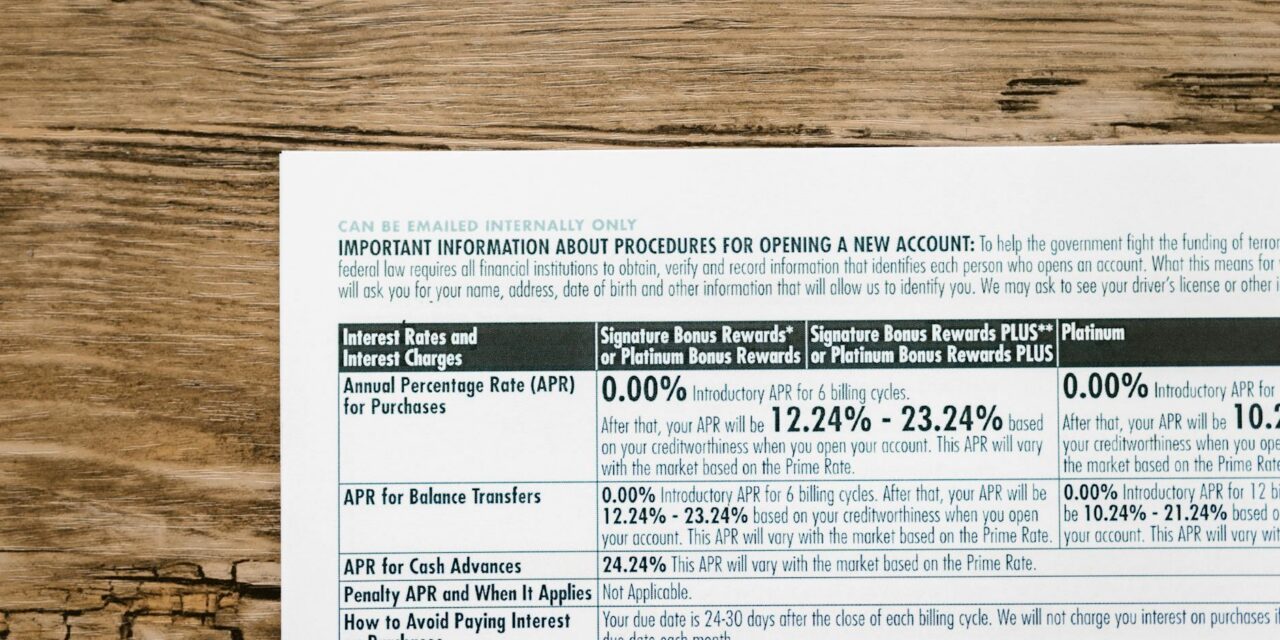

If the theological critique of usury is sound, the reality of contemporary banking should be alarming. In the United States, the Federal Reserve’s policy of historically low rates has been abandoned; today’s benchmark rates hover near 6 % and continue to climb. When a typical 30‑year mortgage jumps from 3 % to 6 %, monthly payments double, pushing home ownership out of reach for millions of families.

The impact ripples beyond housing. New cars—once a modest expense—now require financing at rates that often exceed mortgage interest. Many consumers claim that “a car costs as much as a home and carries double the interest rate,” reflecting the perceived parity between these essential purchases. While precise data are scarce, the lived experience of families burdened by multiple high‑interest loans is undeniable.

High interest rates also force borrowers to allocate a larger share of their income to debt service, leaving less for food, health care, and education. The Federal Reserve’s own data show that when interest rates rise, consumer debt‑to‑income ratios increase sharply, a trend that directly translates into tighter household budgets and heightened financial anxiety.

The result is a society where the promise of “credit” becomes a trap: people are encouraged to borrow, only to find themselves shackled by payments that eclipse their wages. The moral outrage that once surrounded medieval usury now manifests as a systemic crisis of human dignity.

From Housing to Meme Tokens: The Interest‑Driven Flight

When borrowing becomes prohibitively expensive, investors seek alternatives that promise high returns without traditional debt. A recent Kindalame article documented how surging interest rates are pushing capital from real estate into meme‑style cryptocurrencies. The slowdown in the housing market, directly linked to higher mortgage costs, has left many would‑be homeowners searching for speculative outlets.

The article notes that the “rise of meme tokens” is not a benign diversification but a symptom of desperation. Young professionals, unable to afford a down payment, pour savings into volatile digital assets hoping for a quick windfall. This shift illustrates a deeper problem: the financial system’s reliance on interest forces people into speculative bubbles, undermining long‑term stability.

Moreover, the crypto market’s volatility magnifies inequality. Those who can afford to lose their entire investment are typically already affluent, while those who cannot absorb losses end up deeper in debt when speculative bets fail. The cycle—high interest → unaffordable assets → speculative risk → greater financial fragility—reinforces the original sin of usury: extracting value from the vulnerable while enriching the already powerful.

Time Banking: A Human‑Centric Alternative

If interest‑laden finance is a moral disease, what cures exist within our own communities? Kindalame’s exploration of time banking as a utopian solution offers a compelling prototype. In a time‑bank, participants earn “hours” by providing services—childcare, tutoring, gardening—and can spend those hours on others’ services. No money changes hands, and no interest accrues.

Time banking re‑centers the economy on human labor rather than financial capital. By valuing an hour of work equally across professions, it dismantles the hierarchy that interest creates: lenders sit atop borrowers, profiting from the mere passage of time. Instead,

{kind=link}

Trackbacks/Pingbacks